- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Asset Allocation: The Future is not in the Past

Themes from 2023 so far – and what they mean for our industry. This article shares my thoughts on the implications of this year’s themes of inflation volatility, liquidity concerns and deglobalization – and the tools required for navigating these conditions. These include the ability for asset allocators to make and execute decisions more quickly, and greater flexibility for their investment infrastructure.

This article is part of Gary’s ‘Outside-In Thinking’ series of articles on how the asset servicing industry can design solutions and technology that brings clients closer to achieving their objectives. You can also view the article and comment here on LinkedIn. Read more about Gary and see further articles here.

Northern Trust’s role as asset servicer to asset owners and asset managers around the world provides us with a global lens of the investment industry. Through this we gain a view of the market trends impacting our clients, as well as the potential opportunities open to them and key challenges that they and their investors face.

And as I've mentioned previously, part of my job at Northern Trust is to view our business from the ‘outside-in’ through our clients’ eyes. I meet with them, work to understand the challenges they’re trying to solve and collaborate with colleagues to help them achieve that.

So as we reach the halfway point of a year filled with almost continuously-negative headlines and one where the most consensual view seems the ‘consensus is wrong’ it’s a good time to take stock, try to join the dots and assess any connecting themes.

In that spirit, I set myself the task of identifying three key challenges impacting our industry and their implications for asset servicers and how we can help. The first I’ve identified is primarily one facing asset owners/allocators and particularly their Chief Investment Officers (CIOs): the need for operational preparedness for a very different investment landscape than the one we may be leaving behind.

The future is not in the past

‘The world is changing, but my strategy/my portfolio is going to be just fine’ – this may be a little glib, but it looks like the key message from Casey Quirk’s 2023 CIO Sentiment Survey. The majority of CIOs plan no change in allocations despite recognising a generational change in markets and having very little confidence in meeting return targets.

Many have the same investment tilts: to illiquid assets, to the US/US equities, to technology and other things, and that lack of heterogenous exposure creates a significant homogenous risk. Either that – or they are all hoping for a return to pre-pandemic programming, the Washington consensus, global co-operation, ample liquidity, low stable inflation, low rates and high terminal values. However, with regard inflation, a study of history would highlight how rare this actually is. Arnott and Shakernia studied inflation persistence in 14 developed economies from 1970 to 2022.

They found that: “Reverting to 3% inflation… is easy from 4%, hard from 6% and very hard from 8% or more. Above 8%, reverting to 3% usually takes six to 20 years, with a median of over ten years.” So, inflation volatility looks like it’s here to stay for some time.

I’ve been meeting regularly with CIOs in my role for over a year now and asking what their major challenges are. Initially it was the usual suspects: costs, regulation, technology or talent. Last year new frontrunners emerged: liquidity management and performance. The former of course refers to the ability to buy or sell an asset quickly and in large volume without substantially affecting the asset’s price (to fund redemptions, collateral or take advantage of mispricing) – and by the latter, I don’t mean the downturn suffered by many balanced funds in 2022.

I mean something more foundational: the idea an entire generation of investors might need to find new tools, learn new techniques (and unlearn old ones) to succeed in a new market framework. A framework dominated by something few investors have had experience with: inflation and in particular, inflation volatility. And so, my concern, is with the collective idea that what has worked in the past will continue in future. It might, but only if by the past they mean a period ravaged by inflation volatility. And for that, you have to go back to the late ‘60/70’s: a period where there were few PE firms, even fewer PC firms and bonds were known as ‘return-free risk’.

So what are these new tools and techniques? What might asset owners/allocators need to unlearn? Well, the first is the idea that stock markets always go-up over time. They don’t – it depends entirely on the time period in question.

In real terms, according to Ian Hartnet at ASR, it took 30 years to get your money back after 1929, 20 years after 1968 and 15 years from 2000….And it’s only real returns that matter during inflationary periods, as what good is getting your money back if your money has lost its purchasing power? And of all those periods I think the ‘70’s provides the closest parallel, not only because of inflation volatility, but because it started the period with extreme valuations. Sound familiar?

What happened next was a painful period of readjustment, where the market worked off the excess of the previous bull market, and multiples compressed from well above 20x to below 10x and stock indices cycled up and down but effectively went nowhere for 14 years. This is known as a range-bound market and I believe it’s the setup we have in the US, a market that attracts circa 70% of investor capital yet is supported by only 20% of world GDP. (More on mean reversion shortly).

What are the characteristics of a rangebound market? Well, all stocks, as measured by the Index do poorly. But some stocks do well (think stock pickers). The trick is to not confuse the trends of the system (from extrapolating from the whole) with the trends within that system. This helps explain the current divergence between large US tech stocks and markets generally.

As Rob Hagstrom showed back in 2010, between August 1975 and Oct 1982 the Dow started and finished at exactly the same price, yet c.40% of Dow stocks doubled during the period. The stocks that did well were characterised as value, generated high un-levered FCF, paid dividends and had pricing power. It's earnings-growth, not price-to-earnings that do well in these times and given the requirement to have a greater margin of safety (to withstand this multiple compression) identifying value becomes a key active manager character trait.

By the way, in studies of long-term returns, Fidelity Investments concluded that dividends have accounted for 40% of stock market returns since 1930 and 54% during decades when inflation has been high. Moreover, the single most important determinant of long-term (i.e. 10+ years) gains, is starting valuation. According to BAML, “valuation, in terms of normalized P/E has explained 80-90% of returns over the subsequent 10-11 years.” And where do you find value and dividends? Well, it’s not the US.

US stocks make up about 70% of the MSCI Al-World Index. This in a country that represents less than 20% of global GDP and a market I believe is range-bound for a decade (see above). In contrast, Japan, Germany, the UK, France and 19 other countries which represent the vast majority of global GDP, account for less than a third of that index. These markets should do better over the long-term given lower starting valuations. Japan and the UK have experienced multi-decade secular bear/side-ways market, have emerged with low valuations and are either undergoing, or are about to, experience significant reform that should positively impact equity markets.

The Tokyo Stock Exchange, for example, aims to optimise corporate balance sheets, streamline crossholdings and lift book values to above >1. In a market where 50% of stocks trade below book value that’s interesting, especially versus the US where only 3 stocks trade below BV. The UK is even more interesting. The current government seems committed to driving through capital market reforms to not only improve the conditions to list in the UK but also the availability of capital with which to do so

Take pension savings in the UK where over the past 20 or so years the home bias towards UK public equities has fallen from above 50% to below 5%. As regulations were part of that problem, there reforms will be part of the solution and this savings ‘un-lock’ (think $8trn vs FTSE at £2.2trn) could have the potential to do what 401k’s did to the US market after the end of its secular bear-market in 1982.

This to me looks like a potential opportunity for mean reversion. After all, there was a time when Japan was nearly 40% of the index (it’s currently 6%) and the UK (at 3.5%) but was once closer to 10%.

So, by ‘active’, I mean managers that include international exposure as unlike the US where multiples are well above average, some markets like the UK and Japan are well below theirs’ and both provide free options on market-friendly reforms.

I also expand the definition of active to be active buy- and sell-investing, as selling discipline is critical in range-bound markets. And selling can be hard, as human emotion often gets in the way. Hopefully your asset managers are data-driven – and if they are, they could consider using data science tools that can provide nudges to managers based on previous behavioural patterns. These can also be helpful for allocators looking to move away from past performance as a criteria for manager selection – which is redundant if you believe the future looks unlike the past (I’ve mentioned this in a previous article).

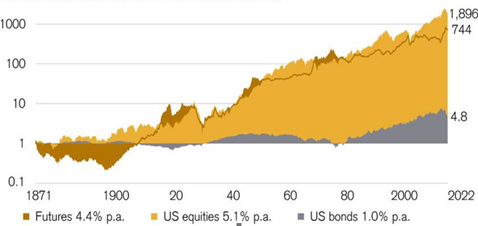

Anyway, equities will likely still dominate the game, but it will be played a little differently than previously: more active, more international and probably more turnover (as buy-and-hold strategies go away for a time). Note that since 1871, equities are the best – most of the time – except during periods of inflation, when commodity futures outperform (brown line below).

Source: The Global Investment Returns Yearbook.

What are the best diversifiers?

The question then becomes: what are the best assets for diversification? Probably not bonds. While bonds have provided equity-like returns since the 1980s, the inflation shock of 2022 meant real bond returns were the worst on record for many countries. And in the inflation ravaged ‘70’s, bonds were known as ‘return-free risk’. Bonds hate inflation. Yes, you get your money back, but what’s the use if it’s lost all its purchasing power? You at least need to protect your capital. So, what are your options?

Cash? Yes, cash now has a risk-free return and goes someway to offsetting inflation. But not all the way….and it’s still a liability and so I’m not sure if it’s a great diversifier in the face of inflation (as purchasing power erodes over time). I would have some invested cash, but I see it more for option or strategic value, as at the end of credit cycles you can often buy distressed assets. As James Aitken is fond of saying, there’s no free lunch in investing, the closest thing is the meal left at the table by worried investors 1. So I would hold cash for strategic reasons. Not to diversify.

I believe investors prefer to own assets not liabilities at the end of the credit cycle, especially assets that are supply constrained and/or have some inflation sensitivity. These worked well in the 1970s. Supply-constrained real-assets like gold, farmland, forestry and even fine art did very well. In today’s terms we would expect more investment into infrastructure, rail, airports, toll-roads and vast amounts into green energy, where industry policy provides an enormous tailwind in the forms of generous subsidies which should lower marginal costs for energy production, putting more pressure on oil prices over time. For evidence of this, construction capex in manufacturing just doubled year-on-year in the US 2.

As the Global Investment Returns Yearbook (mentioned above) shows, commodity futures prove a “diversifier” from an asset allocation perspective – being negatively correlated with bonds, lowly correlated with equities and also statistically a hedge against inflation itself. As the chart above illustrates, commodity futures long-term performance is not far behind equities. (Oil is the only commodity I believe no longer meets these criteria, see above: industrial policy).

I think derivatives will likely grow as an asset class. They’re a way to protect against interest rate volatility, hedge tail / factor risks, but also amplify returns and generate income. We are finding even conservative clients, for example, doing covered call writing and then reinvesting the premia in short-dated treasuries to optimise those returns further still. And I think balance sheets will become reappraised as, essentially, an asset class. This could be perhaps the biggest trend for the new world, especially if competition for capital remains.

More allocators will look to optimise their balance sheet as a way to improve returns, improve portfolio liquidity and generate outperformance without tilting. And given the size of the numerator, the additional alpha could be significant. We expect traditional treasury, financing, collateral and liquidity functions will be centralised, injected with risk-taking authority and roll directly into the CIO. The job is then to identify the most optimal use of an asset across collateral, financing and liquidity channels.

Future strategies require the right structures

If you want different results, do different things. Easy to say, hard to do. That said, I worry that the majority of the world’s asset allocations are tilted the same way. Of course, that’s fine if we return to pre-pandemic programming. But if we don’t, we will need new models and new assets to navigate the new regime and allow savers to afford their retirement.

I appreciate what I say above might seem provocative – but that’s the point: to rattle the cages of complacency and force us to challenge our assumptions. Change is hard, and innovation is often seen as incompatible with job security – making consensus an easier, safer and more popular position. But the thought process at least, is necessary, even if you return to where you started from.

Another future state requirement is for liquidity solutions or cash-buffers to be more opportunistic, when mispricing occurs, as they inevitably do at the end of a credit cycle and/or when inflation/rates volatility causes extreme pricing movements. “When you sell in desperation, you always sell cheap” (Peter Lynch).3

Expecting a broader range of market and economic outcomes is now a base requirement for allocators. Inherent in this idea, is the need to have model flexibility, not just of thought but of relationships and critically, of operations. Strategy needs the right structure to succeed. And in future, these structures will need to become more flexible, more interoperable, open and data-source agnostic, in order to meet the future state requirements of flexibility, agility, resiliency and scale.

The next step: and how we can help: Platforms As a Service

We (Northern Trust) aim to provide platform capability, or “Platforms As a Service”, for these activities that organisations will access. So: new assets, new markets, new geographies and more frequent turnover in liquid assets will mean that their operating models will need to be more flexible, agile, interoperable and offer greater data transparency.

I also think we’ll see a move away from a rigid ‘bottom-up’ approach to asset allocation towards a more flexible, holistic top-down one with greater instrument diversity (think derivatives) and a new revenue line coming from balance sheet optimisation.

In short, organisations will need to ensure their ‘strategy fits with their structure’ – that they have an operating and data model in place that can meet the future needs of the investment team.

This probably means that asset owners/allocators will require less fixed-costs, have more reliance on strategic partners and, as mentioned above, data models that are agnostic and able to harmonise across all public and private data (with look-through capability). The latter will provide CIOs and Chief Risk Officers with a total portfolio view – enabling them to identify their risks in real time and buy protection and/or position accordingly.

1 Source: James Aitken, Notes from a Small Island

2 Source: United States Census Bureau

3 Peter Lynch: One Up On Wall Street: How to Use What You Already Know to Make Money in the Market, April 2000

_____________________________

NEITHER THE INFORMATION NOR ANY VIEWS EXPRESSED CONSTITUTES INVESTMENT ADVICE AND IT DOES NOT TAKE INTO ACCOUNT THE SPECIFIC INVESTMENT OBJECTIVES, FINANCIAL SITUATION AND THE PARTICULAR NEEDS OF ANY SPECIFIC PERSON WHO MAY VIEW THIS MATERIAL.

These are my own personal views, not those of my employer. This report is not intended for retail customers. Any further disclosure, use, distribution, dissemination or copying of this report or any of the information herein is strictly prohibited. The information in this report has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Any opinions expressed herein are subject to change at any time without notice. Any person relying upon information in this report shall be solely responsible for the consequences of such reliance. This report is provided for informational purposes only and does not constitute legal, tax or other advice nor does it constitute an offer or solicitation to purchase or sell any security, commodity, currency or other product. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining advice from their own advisors. Internet communications are susceptible to alteration and Northern Trust shall not be liable for the message if it has been altered, changed or falsified.

Meet Your Expert

Gary Paulin

Head of International Enterprise Client Solutions

As Head of International Enterprise Client Solutions, Gary focuses on strengthening Northern Trust's relationships with key clients across Europe, Middle East, Africa and Asia-Pacific at the highest levels of their organisations, principally their chief investment officers and chief executive officers.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. This material is directed to professional clients (or equivalent) only and is not intended for retail clients and should not be relied upon by any other persons. This information is provided for informational purposes only and does not constitute marketing material. The contents of this communication should not be construed as a recommendation, solicitation or offer to buy, sell or procure any securities or related financial products or to enter into an investment, service or product agreement in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful. This communication does not constitute investment advice, does not constitute a personal recommendation and has been prepared without regard to the individual financial circumstances, needs or objectives of persons who receive it. Moreover, it neither constitutes an offer to enter into an investment, service or product agreement with the recipient of this document nor the invitation to respond to it by making an offer to enter into an investment, service or product agreement. For Asia-Pacific markets, this communication is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author's employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP, Northern Trust Global Services SE UK Branch and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT, are authorised and regulated by the UK’s Financial Conduct Authority. The Northern Trust Company, London Branch and Northern Trust Global Services SE UK Branch are also authorised and regulated by the UK’s Prudential Regulation Authority. Not all of the products and services mentioned within this material are authorised and regulated by the UK’s Financial Conduct Authority or UK’s Prudential Regulation Authority. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651) (NTGL)/Northern Trust Fiduciary Services (Guernsey) Limited (29806) (NTFSGL)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) (NTIFASGL) are licensed by the Guernsey Financial Services Commission. Registered Office: NTGL/NTFSGL -Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. NTIFASGL - Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3QL. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386). Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.